The pay calculators are used to determine your net income by deducting federal taxes (10-37%), state taxes (0-13% depending on location), FICA taxes (7.65%), and any local deductions from your gross salary, and they have great differences in all 50 states.

Have you ever questioned yourself about why you earned more in Texas with your $75,000 salary? You are making $58,199, but in California, you are making $51,224? The disparity, which is almost $7,000 annually, is determined by how the federal, state, and local taxes add up depending on the place of work. A US pay calculator carefully cuts through all this detail and lets you look at your real take-home pay in a few seconds by considering where you are, your filing status, and deductions.

This guide examines how these tools function in various states and explains why, in 2026, they will be crucial for financial planning.

What Is a Pay Calculator, and Why Do You Need One?

A pay calculator is software that calculates the net deductions and taxes payable on your gross salary, which is then used to calculate the net salary you will take home at the end of the fiscal period. Computerized calculators instantly calculate federal withholding, state tax, FICA payments, and allowances such as retirement or health insurance, disposing of hours of arithmetic.

The US Internal Revenue Service estimates that about 75% of taxpayers get refunds with an average payment of $3,000 per year, which is a result of over-withholding. You can avoid this by having a better-designed W-4 withholding calculator to maximize your paycheck over the year; hence, you do not lend the government your money interest-free.

Step-by-Step Guide to How Pay Calculators Process Your Data

The modern net pay calculator tools adhere to the systemic process:

Step 1: Calculation of Gross Income

The pay-type calculator takes the value of a salary that you have provided (annual, monthly, or hourly) and adjusts it to the frequency of the relevant pay period.

Step 2: Pre-Tax Deductions

The tool deducts before any applicable taxes are paid out pre-tax contributions, such as deferrals to 401(k) plans, HSA contributions, deposits to a traditional IRA, and health insurance premiums paid by an employer. These inferences reduce your taxable income.

Step 3: Withholding of Federal Tax

The system uses the present tax brackets of the IRS, using your information on your 2026 Federal Income Tax calculator. These include 10% on income down to $12,400 (single filers) to 37% on income over $640,600.

Step 4: FICA Tax Calculation

The FICA calculator part will be used to pay the obligatory payroll taxes, namely 6.2% back to Social Security, which has a limit of $184,500 in earnings in the year 2026, and 1.45% back to Medicare, which has no limit. High taxpayers are required to pay an extra 0.9% Medicare surtax on income over $200,000 for single filers.

Step 5: State and Local Taxes

It is the place that counts the most. A US state tax calculator uses the tax structure of your state, either a flat rate, progressive, or nonexistent tax structure.

Step 6: Post-Tax Deductions

Lastly, the calculator deducts after-tax savings such as Roth 401(k) contributions, wage garnishments, or charity, and gets your net salary.

State-by-State Tax Differences: How Geography Affects Your Pay

The United States is based on peculiar taxation in which the result of your paycheck is largely determined by the area of living and labor. Whereas federal taxes are consistent throughout the country, local and state taxes bring about a pronounced disparity in payout to take home.

Zero State Income Tax States (2026)

9 states do not have any state income tax: Alaska, Florida, Nevada, New Hampshire, South Dakota, Tennessee, Texas, Washington, and Wyoming. The citizens of these states pay taxes to the federal government and FICA only, and maximize the amount they bring home in their wages.

Progressive Tax States

The majority of states have a graduated tax structure equivalent to the federal structure. The highest top marginal rate is in California, at 13.3% on incomes over 1 million. The highest rate in New York is 10.9, and the highest in Hawaii is 11.

Flat Tax States

In a few states, there is no consideration of income: North Carolina (3.99%), Indiana (2.95%), Illinois (4.95%), Kentucky (3.5%), Massachusetts (5.0%), Michigan (4.25%), and Pennsylvania (3.07%).

Notable 2026 Tax Changes

In 2026, Georgia will lower the flat income tax rate to 5.09% (as compared to 5.19% in 2025), then reduce it by 0.10% each year until it reaches 4.99%. The state of Ohio shifted to a flat rate of 2.75% tax on income over $26,050, whereas the tax on individual income in the state of Mississippi was dropped by 4.4, giving it 4%.

Real-World Comparison: Equal Pay, Equal States

To reflect the changes in your gross-to-net salary conversion in the United States of America, which are dramatic due to location, have a look at the conversion of a single filer with a salary of $75,000 a year after normal deductions:

| State | State Tax Rate | Annual State Tax | Federal + FICA | Total Taxes | Take-Home Pay |

| Texas | 0% | $0 | $11,063 + $5,738 | $16,801 | $58,199 |

| Indiana | 2.95% (flat) | $2,213 | $11,063 + $5,738 | $19,014 | $55,986 |

| North Carolina | 3.99% (flat) | $2,993 | $11,063 + $5,738 | $19,794 | $55,206 |

| California | ~9.3% | $6,975 | $11,063 + $5,738 | $23,776 | $51,224 |

| New York | ~6.5% | $4,875 | $11,063 + $5,738 | $21,676 | $53,324 |

Source: Tax Foundation 2026 State Tax Rates and IRS Revenue Procedure 2025-32

Key insight: The difference between Texas and California amounts to $6,975 annually—nearly $581 per month. This represents a 9.3% reduction in purchasing power simply due to state tax policy.

Effective Pay Calculator Use: Professional Advice

To be as close as possible to any US pay calculator:

- New W-4 every year: Your taxes and personal situation shift.

- Add all the tax-deductible items: 401(k), FSA, HSA, and payment of insurance premiums are excluded from taxable income.

- Check your pay rate: Weekly, semi-monthly, bi-weekly, and monthly rates differ by a great margin.

- Enter exact location: It is necessary not only to choose the state but also the city to be accurate on local taxes.

- Take into consideration changes in between: New job, raise, or relocation will have to be recalculated.

- Look at the end-of-year outcomes: Compare calculations by the calculator to the actual outcomes (W-2) and then update the withholding in the future.

The paycalculator.ai can make this process a little simpler by keeping tax tables current and accommodating all 50 states and local jurisdictions so that your computation is current under the tax laws of 2026.

Common Pay Calculator Mistakes

Mistake #1: Using Old Tax Year Data

Solution: Always use a current calculator as of 2026, with updated brackets and FICA caps.

Mistake #2: Ignoring Local Taxes

Solution: Go into your particular city, but not merely state, particularly Pennsylvania, Ohio, Maryland, and New York.

Mistake #3: Ignoring Pre-Tax Benefits

Solution: Incorporate all 401(k), HSA, and insurance deductions—these are the factors that have a major influence on the take-home pay.

Mistake #4: Confusing Gross vs. Net When Budgeting

Solution: Never budget on the gross salary amounts but on the net income.

Mistake #5: Failing to Recalculate When Life Changes

Solution: What you do is marriage, children, home purchase, and changes in jobs; all these mold your tax position.

Best Salary Calculator Solutions for Payroll Accuracy

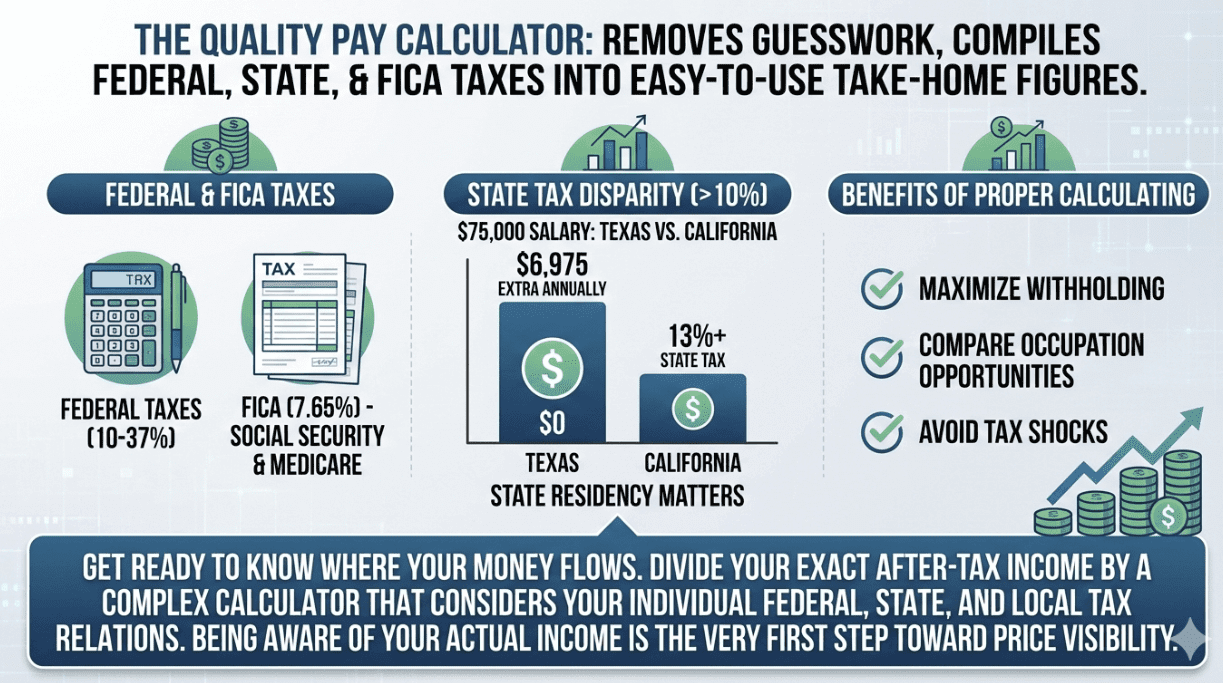

The quality pay calculator removes the guesswork and compiles the federal taxes (10-37%), state taxes (0-13%+), and FICA (7.65%) into easy-to-use take-home figures. State residency brings about a disparity above 10%—a $75,000 salary in Texas earns $6,975 extra annually as compared to the same salary in California. Proper calculating is a way of maximizing withholding, comparing occupation opportunities on a comparable level, and steering clear of tax shocks.

Get ready to know where your money flows. Divide your exact after-tax income by a complex calculator that considers your individual federal, state, and local tax relations—since being aware of your actual income is the very first step toward price visibility.

FAQs:

Q1: How Often Should I Recalculate My Take-Home Salary?

Recalculate when your life undergoes any changes: marriage, children, change of jobs, change of residence, or an increase or decrease in retirement contributions. Recalculate also once a year at the time that the IRS revises tax brackets and the FICA limit, since the rate of 2025 will not align with the tax law in 2026.

Q2: Do the Pay Calculators Include Local City Taxes?

City-based quality calculators contain local taxes in these cities. Other sources impose municipal taxes on top of state rates on top of San Francisco (1.5%), Philadelphia (3.8398), and New York City (up to 3.876%). It is important to know the particular city you are in.

Q3: Is a Pay Calculator Available With Hourly Pay?

Yes. The majority of the calculators consider both hourly workers and salaried workers. Enter rate/hours per pay period—the tax treatment is the same. Bear in mind that greater financial compensation packages include overtime (more than 40 hours per week), which is generally paid at 1.5 times your standard wages, which has an impact on your gross earnings and withholding.